Page 205 - UBP - IR2020

P. 205

FINANCIAL STATEMENTS

Notes to the financial statements

For the year ended June 30 2020

THE GROUP

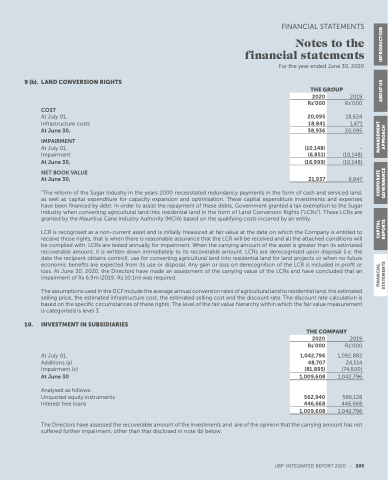

(10 148) (10 148) 9 9 947

9 (b) LAND CONVERSION RIGHTS

2020

Rs’000

20 095

18 841

38 936

(10 148) (6 851)

(16 999)

21 937

COST

At July 01 Infrastructure costs At June 30 IMPAIRMENT

At July 01 Impairment At June 30 NET BOOK VALUE At June 30 2019 Rs’000

18 624 1 1 471 20 095

-

“The reform of of the the the Sugar Industry in in the the the years 2000 necessitated redundancy payments in in the the the form form of of cash and and serviced land as as well as as capital capital expenditure expenditure for capacity expansion and and optimisation These capital capital expenditure expenditure investments and and expenses have been financed by debt debt In order to to assist the the the repayment of these debts Government granted a a a a a a a a tax exemption to to the the the Sugar Industry when converting agricultural land land into residential land land in in in the form of Land Conversion Rights (“LCRs”) These LCRs LCRs are

granted by by the the Mauritius Cane Industry Authority (MCIA) based on the the qualifying costs incurred by by an an an entity LCR is is is is recognised as as as a a a a a a a a a a a a non-current asset and is is is is initially measured at at at fair value at at at the the date on on which the the Company is is is is entitled to receive receive those rights that that is is when there is is reasonable assurance that that the the the LCR will

will

be received and all the the the attached conditions will

will

be complied with LCRs are

tested annually for impairment When the the carrying amount of the the asset is greater than its estimated recoverable recoverable amount amount it it it is is is written down immediately to its recoverable recoverable amount amount LCRs are

derecognised upon disposal (i e e e e e e e e e e e e e e e the date the recipient obtains control) use for for converting agricultural land land land into residential land land land for for land land land projects or or or when no future economic benefits are

expected from fits its use or or or disposal Any gain or or or loss on on on derecognition of o the LCR is is included in in in profit or or or loss At June 30 2020

the the the Directors have have made an an an assessment of of the the the carrying value of of the the the LCRs and have have concluded that an an an impairment of Rs Rs 6 9m (2019: Rs Rs 10 1m) was required The assumptions used in in the the the DCF include the the the average annual conversion rates of agricultural land land to residential land land the the the estimated selling selling price the the the estimated estimated infrastructure cost cost the the the estimated estimated selling selling cost cost and the the the discount discount rate rate The discount discount rate rate calculation is is is based on the the the the specific circumstances of of these rights The level of of the the the the fair fair value value hierarchy within which the the the the fair fair value value measurement is is is categorised is is is level 3 10 INVESTMENT IN IN SUBSIDIARIES

At July 01 Additions (a) Impairment (c) At June 30 Analysed as follows: Unquoted equity instruments Interest free loans

2020

Rs’000

1 042 796

48 707

(81 895)

1 009 608

562 940

446 668

1 009 608

THE COMPANY

2019 Rs’000

1 092 882 24 514 (74 600) 1 042 796

596 128 446 668

1 042 796

UBP INTEGRATED REPORT 2020

-

205

The Directors have assessed the the the the recoverable amount amount of of the the the the investments and are

of of the the the the opinion that the the the the carrying amount amount has not suffered further impairment other than that disclosed in note (b) below FINANCIAL CAPITAL CORPORATE MANAGEMENT STATEMENTS

REPORTS GOVERNANCE APPROACH

ABOUT US INTRODUCTION